EdChoice Public Opinion Tracker: Top Takeaways April 2021

There appears to be light at the end of the 2020-21 tunnel. As one of the most disruptive school years ever draws to a close, many parents and educators are considering what comes next. COVID-19 has forced families to adapt to new rituals and expectations. It remains to be seen exactly how much parents want education to return to pre-pandemic normal. With massive federal aid assisting schools, leaders debate how to best use school resources to help students in the summer and in the next school year. State legislatures introduced a record number of school choice bills this session, and the next couple school years will see educational freedom expanded to more kids across the country.

That was the backdrop for the release of our April wave of the EdChoice Public Opinion Tracker. Morning Consult conducts a monthly tracking poll based on a nationally representative sample of adults 18 years and older (N = 2,200, in the field April 16-26). With additional sampling, we obtained responses from a total of 1,134 parents of school-aged children so we can report more reliable information about parent subgroups by demographic.

WHAT WE LEARNED: Americans are more optimistic about classroom safety, public COVID-19 responses, and the overall direction of education. A growing share of parents think time currently spent on standardized testing is appropriate. Interest in school choice policies and non-traditional forms of education remains high. Learning pod interest in particular may be experiencing a slight resurgence.

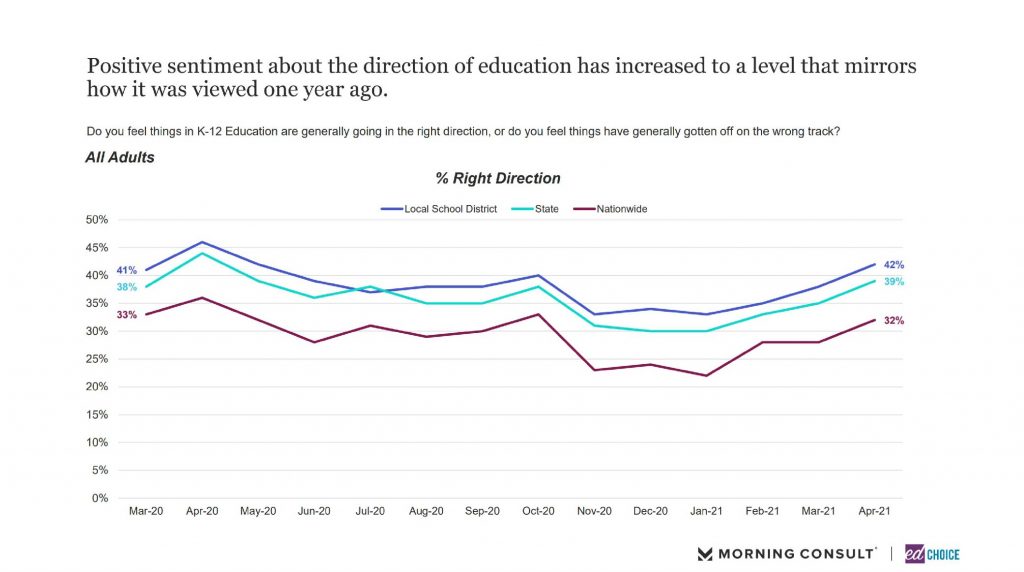

1. Americans continue to think K-12 education is moving in the right direction. After November’s COVID-19 surge saw a drop in optimism, adults are regaining confidence in K-12 education. In fact, we found that optimism about education on national, state, and local levels were identical to those we saw 12 months ago, and they are the highest ratings since October.

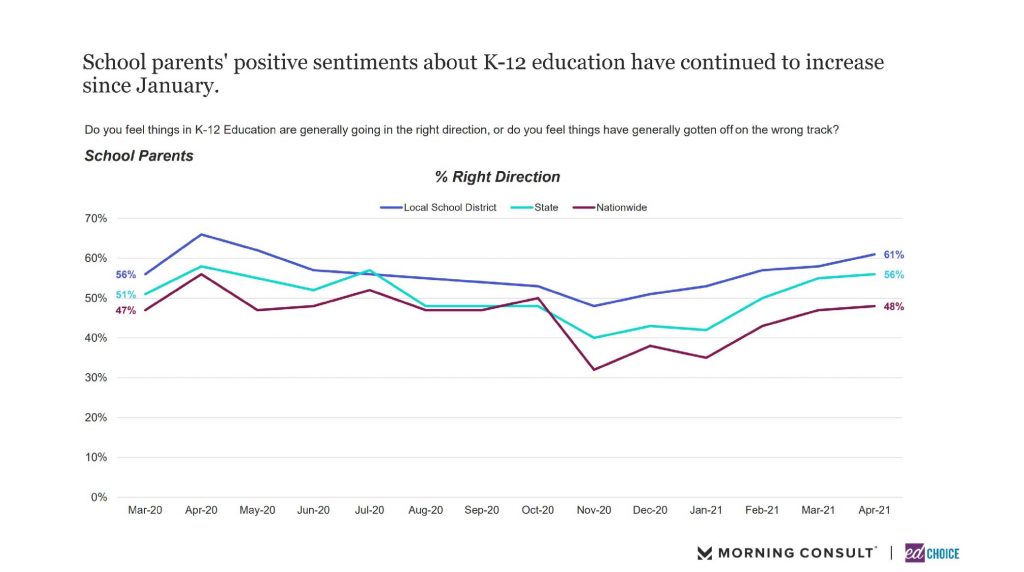

Parents remain significantly more positive about K-12 education than the broader population, and while the climb has not been as steep as that of adults as a whole, their optimism also is rising.

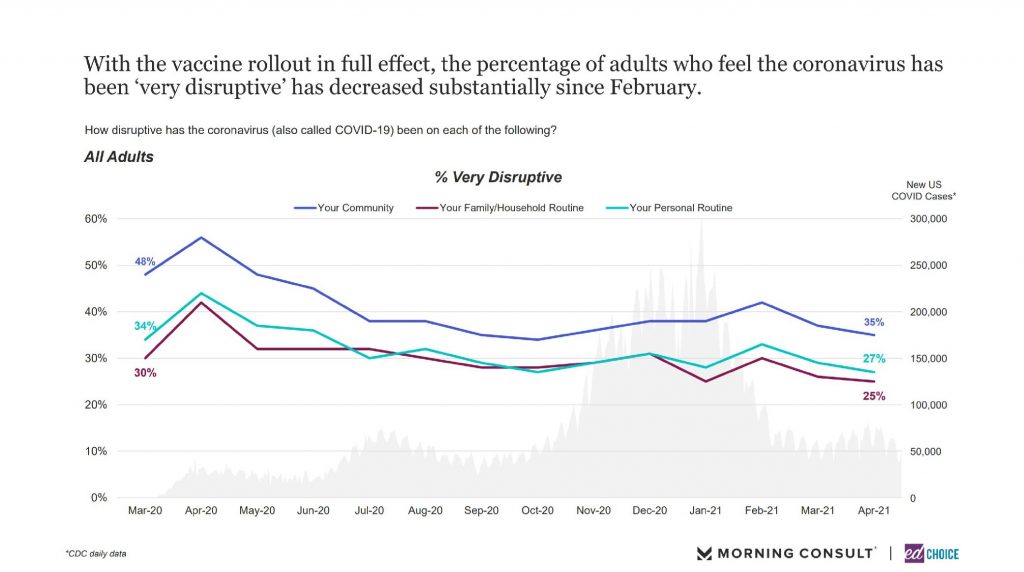

2. People feel less disrupted by the pandemic now than they have since lockdowns and closures began happening back in March 2020. In April, about a quarter of adults said COVID-19 is “very disruptive” to their personal or household routines. These numbers are the lowest they have been since we began asking questions about the COVID-19 pandemic last March. Thirty-five percent of adults said the pandemic is disruptive to their communities, the lowest share since October when 34 percent saw their communities as very disrupted.

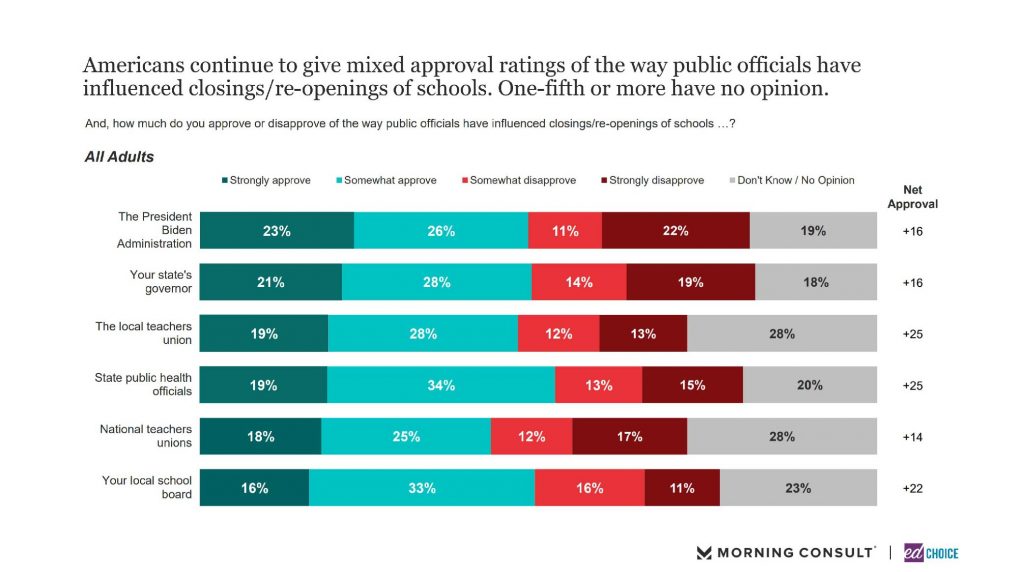

3. Opinion on public institutions’ influence on school closures have improved slightly since March. Among all adults, total approval for various public institutions regarding their relationship with school closure and reopening policies saw slight increases since the last month, between one and four percentage points for each, with the Biden administration seeing the biggest improvement. Somewhat significant shares of adults indicated they did not have an opinion, however.

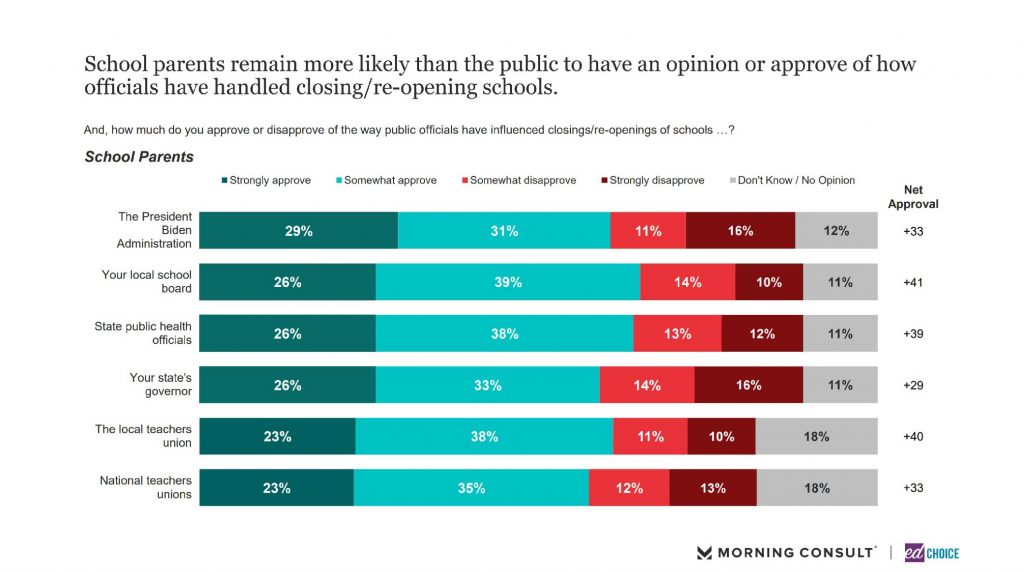

School parents are significantly more positive about how public institutions have managed school closure and re-opening policies, with total approval exceeding total disapproval by at least 29 percentage points for every entity, a greater margin than any category among all adults, though these ratings did not increase noticeably from March.

Among both the general population and school parents, total approval for teachers unions are positive but rank among the least-popular institutions with regard to school closure and re-opening policies.

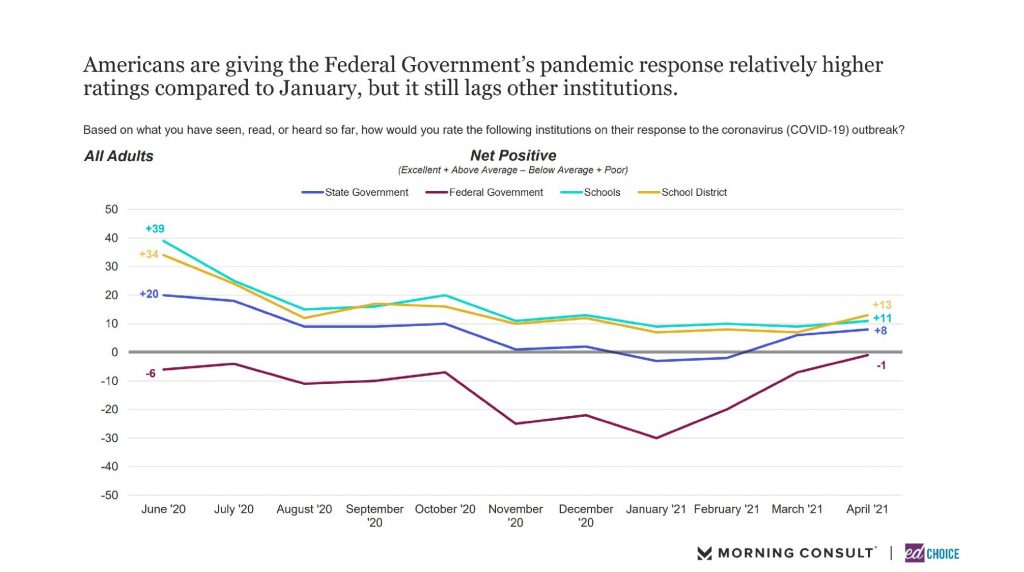

Among the general population, the net positive rating for state and federal governments regarding their pandemic responses have been on the rise since January. Federal government remains the lowest-rated institution, but its total positive rating nearly exceeded its total negative rating for the first time since we began asking this question in June. School districts rated higher than schools for the first time since September.

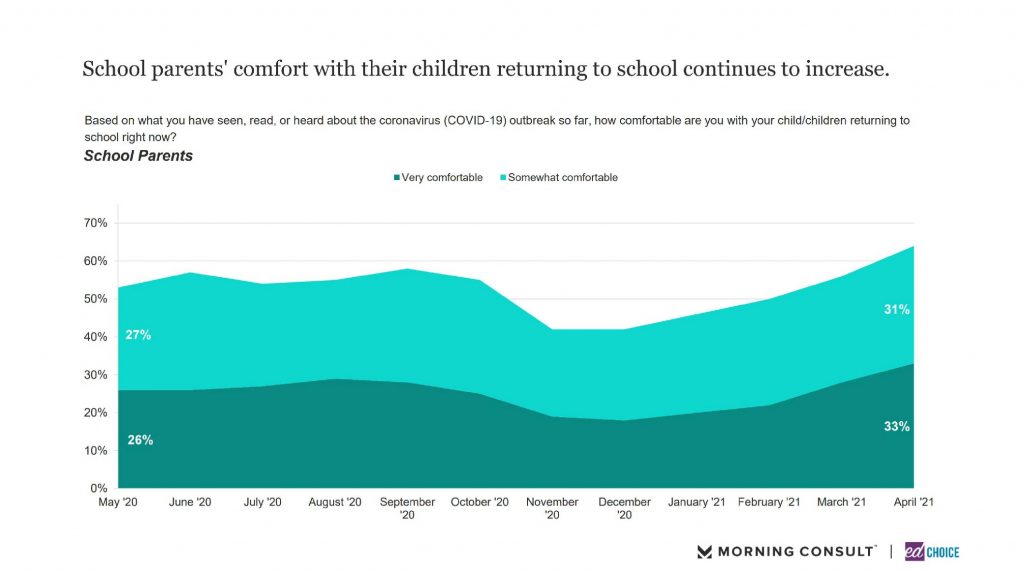

4. Comfort with in-person education continues to climb. In February, the share of parents saying they were at least somewhat comfortable with their children returning to school reached 50 percent for the first time since October. In the two months since, total comfort has risen rapidly, hitting nearly two-thirds in April. Notably, this is the first time “very comfortable” exceeded “somewhat comfortable” since August.

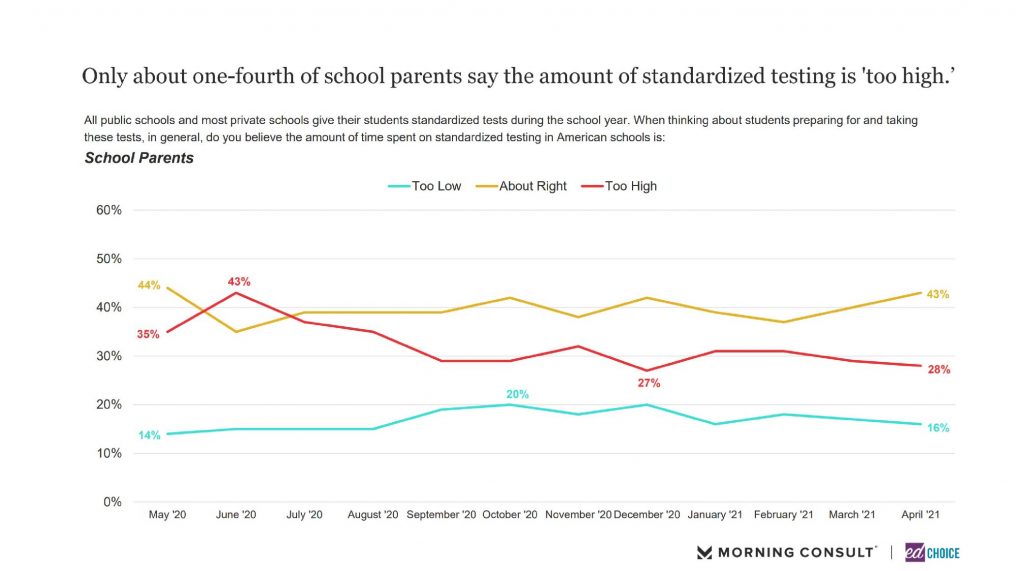

5. A rising share of parents think time spent on standardized testing is “about right.” Both March and April have seen declining shares of parents who think too much or too little time is spent on standardized testing, with 43 percent saying the amount of time spent on testing is “about right.”

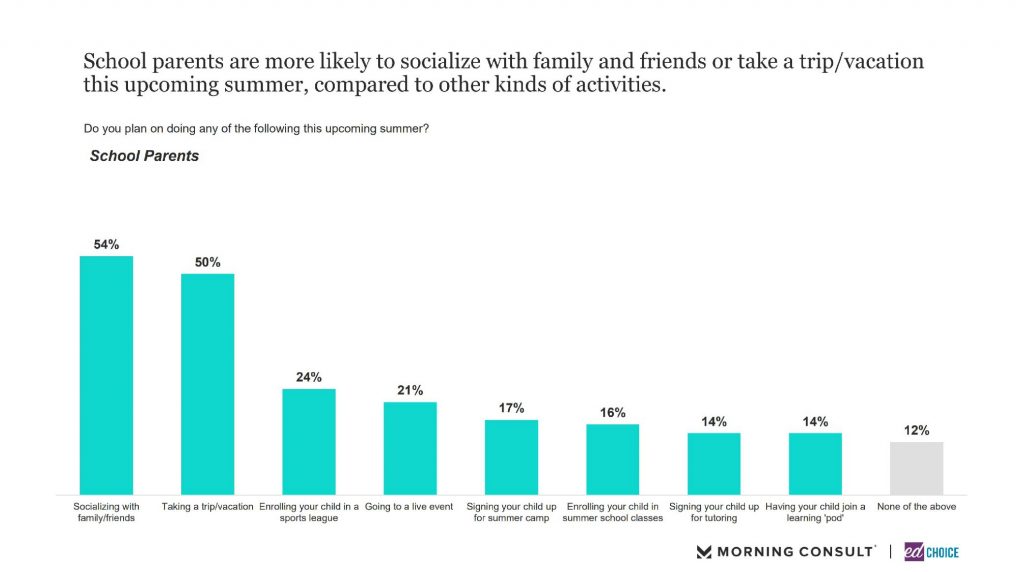

6. About one in seven parents plan to have their child participate in academic activities outside of a traditional school setting this summer. With much discussion about schools expanding summer school offerings to make up for any learning losses experienced during COVID-19 and school closures, we asked parents how they were planning to spend their summers. Fourteen percent of parents said they planned to enroll their children in tutoring or a learning pod.

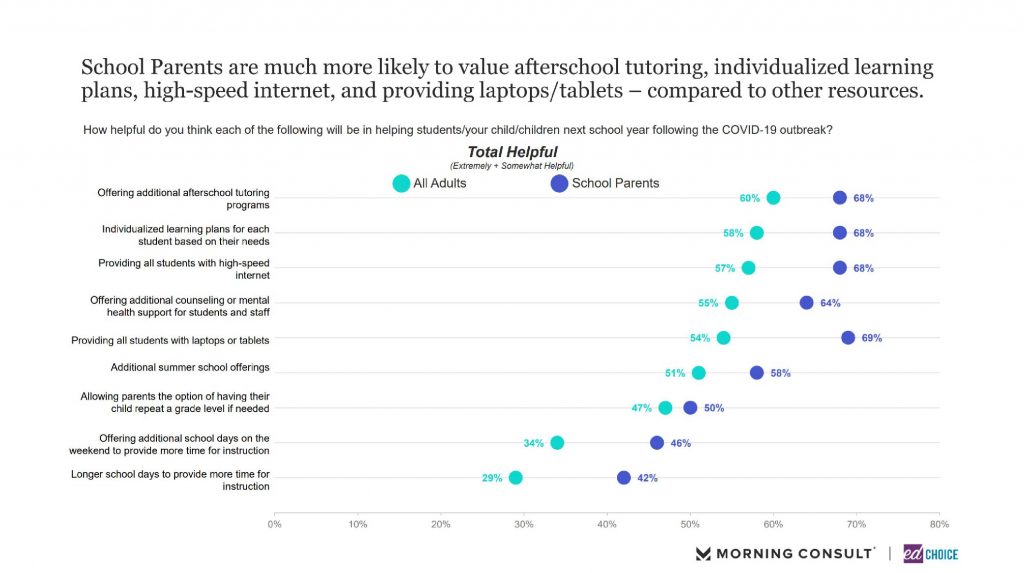

7. Parents are optimistic about various educational tools’ ability to help students thrive next school year. We proposed nine different resources a school might offer to help students next school year in light of the pandemic outbreak. School parents consistently were more likely to say a given idea would be helpful for students, with particularly high preferences for laptops, high-speed internet, afterschool tutoring, and individualized education. Grade repetition, optional school on weekends, and longer school days did not receive the same confidence.

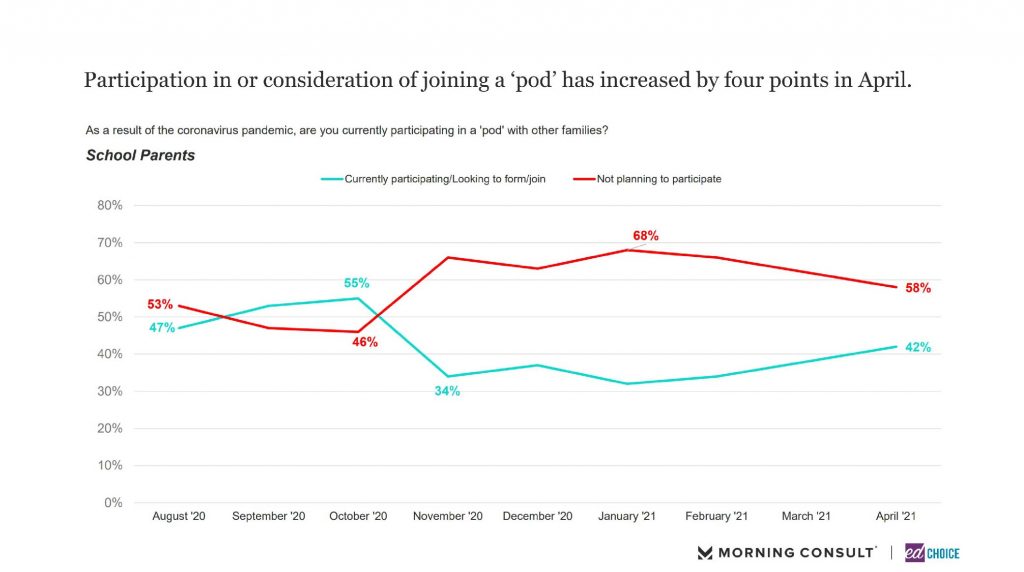

8. Interest in learning pods is at its highest level since October. Pods appeared especially appealing to parents in early fall, peaking in October at 55 percent of families saying they were in or looking to be in a pod. Just one month later, that number dropped to 34 percent, and pod interest remained in that range for the next several months. Since January, however, there has been a small but steady rise in the share of parents saying they are in or want to be in a pod, climbing to 42 percent in April. As has been the case since November, the share of parents saying they are in a pod is nearly equal to the share of those indicating they are not in but are looking to join a pod.

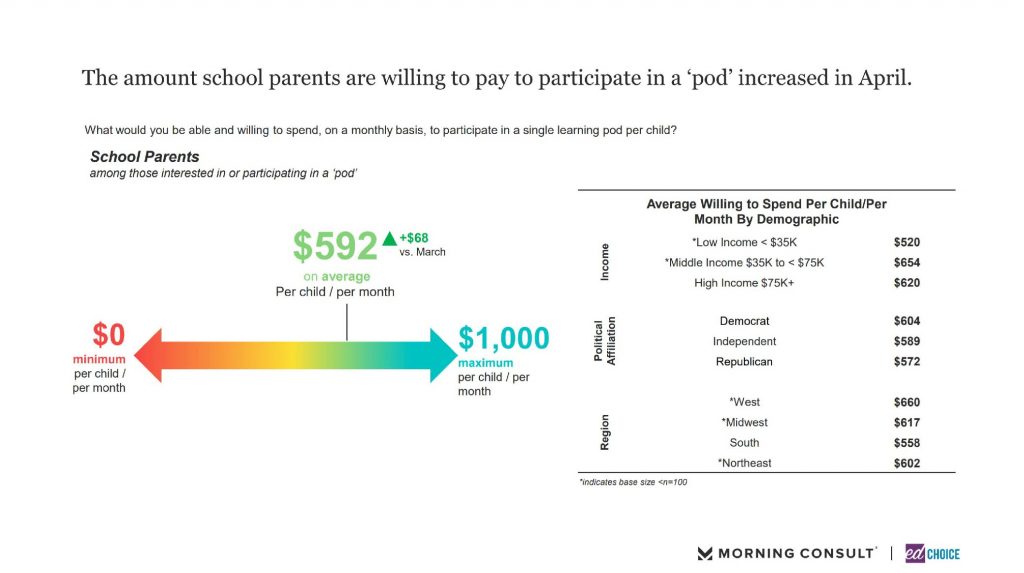

Pods usually require families to contribute some fees to participate. We ask parents how much money they would be willing to pay to participate in a pod. In April, the average parent in or interested in a pod said they would be willing to pay $592 per child per month. To put that number into perspective, that is $169 more per month higher than the average parent indicated in January. In other words, the willingness to pay for pods has risen 40 percent since the beginning of the calendar year. This rise could indicate that the intensity of desire for pods is rising in addition to the quantity of people who want them. For a more in-depth take on what parents and educators think about pods, check out this recent blog post.

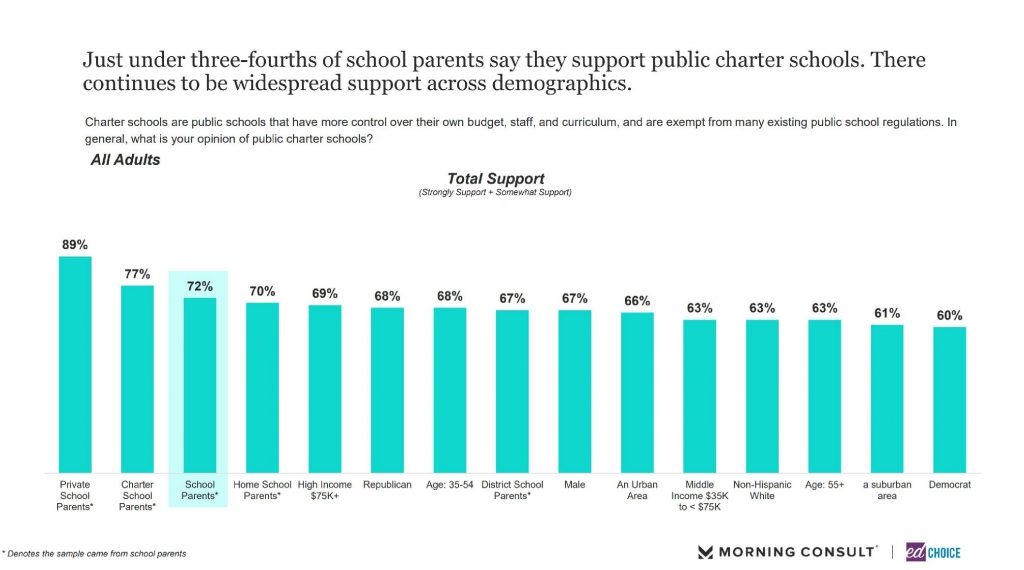

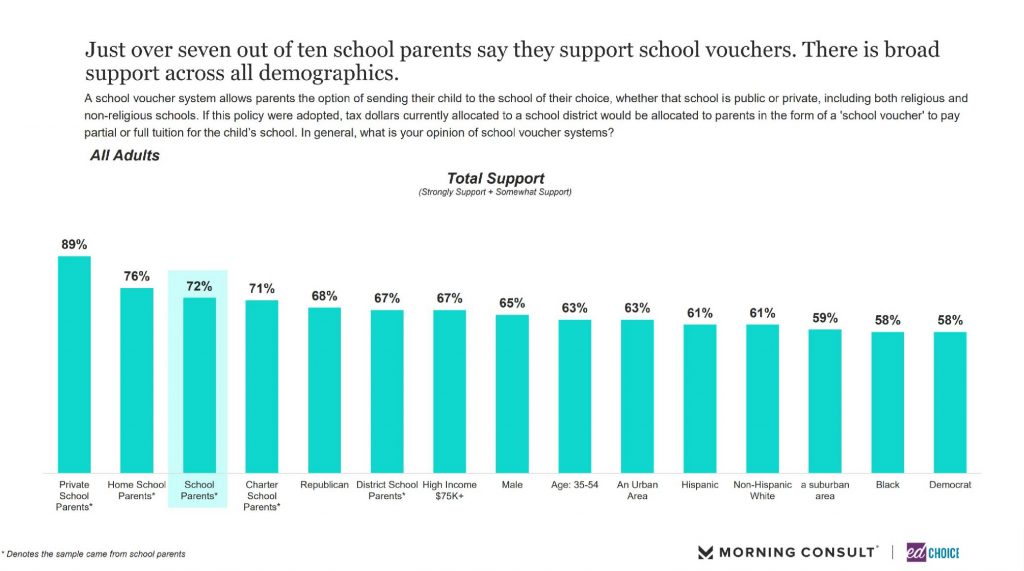

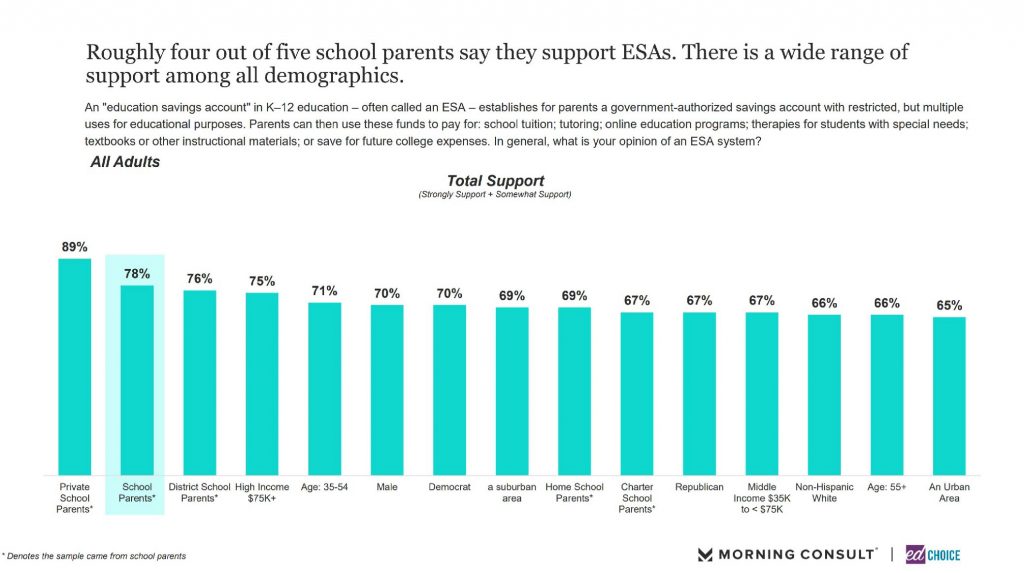

9. Support for school choice programs remains high, especially among parents. When provided a definition, 72 percent of school parents support charter schools and voucher programs, and 78 percent support education savings accounts (ESAs). Each of these numbers are essentially steady with March’s results.

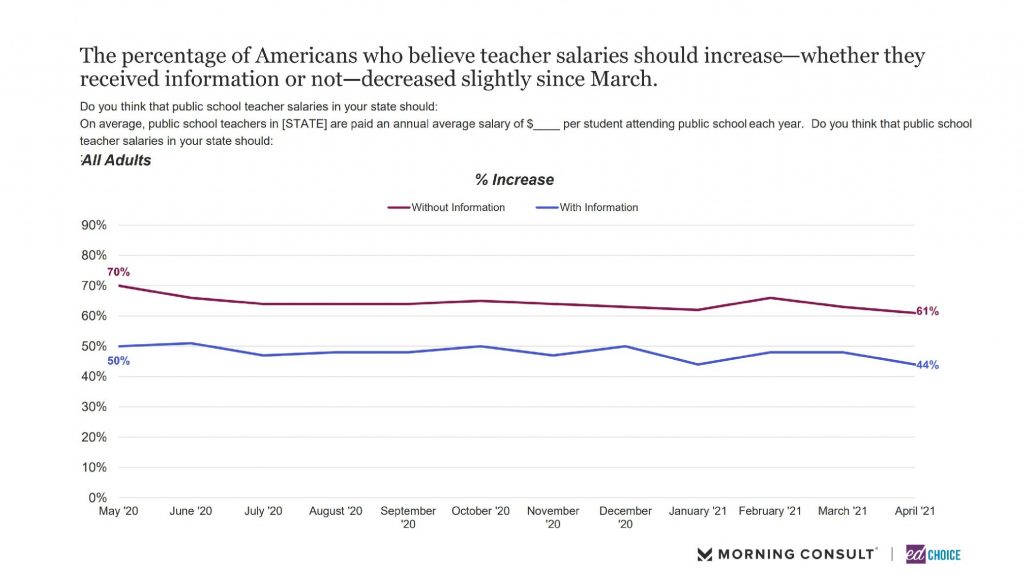

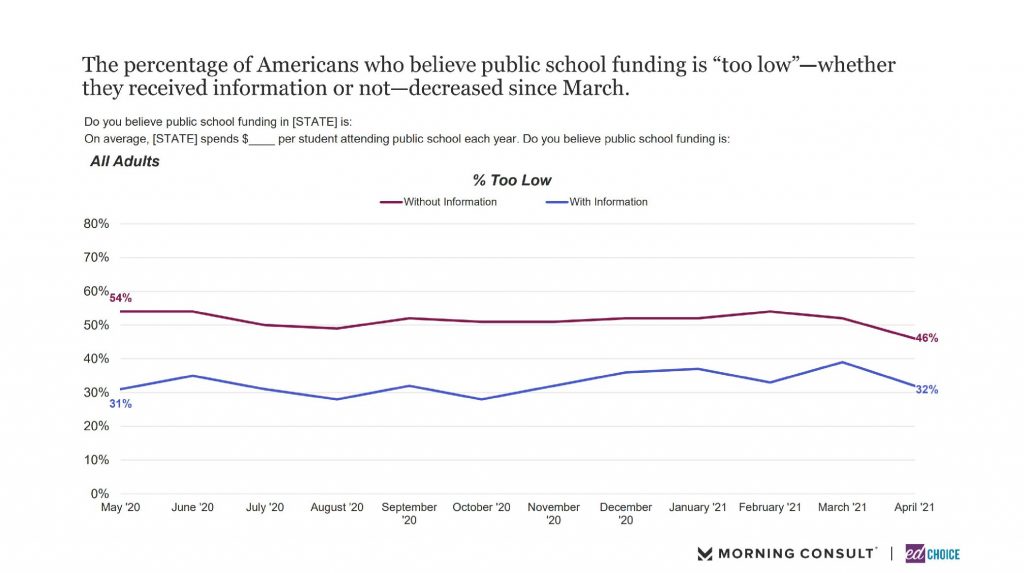

10. There has been a slight decrease in the belief that school funding and teacher salaries should increase. We ask two split-sample survey questions about school funding. One question asks all adults if they think public school spending is too low, and some are presented with actual current per-pupil expenditures in their state. For both those with and without spending information, fewer respondents indicated they thought school spending was too low compared to the March survey, a decline of seven and six points respectively.

Similarly, we ask if teacher salaries should increase, with some respondents seeing the average teacher salary in their state. While not as stark as the responses to the school funding question, there has been a noticeable decline in the share of responses saying teacher salaries should increase.