EdChoice Public Opinion Tracker: Top Takeaways December 2021

Fall 2021 began with Delta and ended with Omicron. Nearly two years after the novel coronavirus disrupted schools across the country, its variants still pose challenges to K–12 education.

We began our monthly Public Opinion Tracker to identify sentiment at different snapshots in time. Because this December 2021 edition of our tracker was in the field December 14–16 (n = 2,200, including 1,325 school parents with an oversample of 700 school parents), we only were able to capture the earliest stages of any concerns about the Omicron variant.

Still, as cases were back on the rise, we were able to notice a few changes of opinion, and the answers that changed little from November may be revealing in their own way.

Our polling is not restricted to COVID-19 matters, of course. The December 2021 wave includes some new questions, the return of some old interesting questions, and plenty of insight into America’s K–12 experience right now. You can check out the complete results at our tracker website here.

Before we get into the key findings, you can visit this page on the EdChoice Public Opinion Tracker site for access past polling reports and briefs as well as demographic crosstabs and questionnaires. We also provide a more in-depth description of our methodology. Over the past two years, we have been cataloging education-related polls and surveys during the pandemic. Our K–12 Education Polls Archive is updated on a rolling basis, roughly a few times each month. Please don’t hesitate to let us know if we are missing any surveys, or if there are accidental errors.

Here are the six most interesting things I noticed about December’s polling:

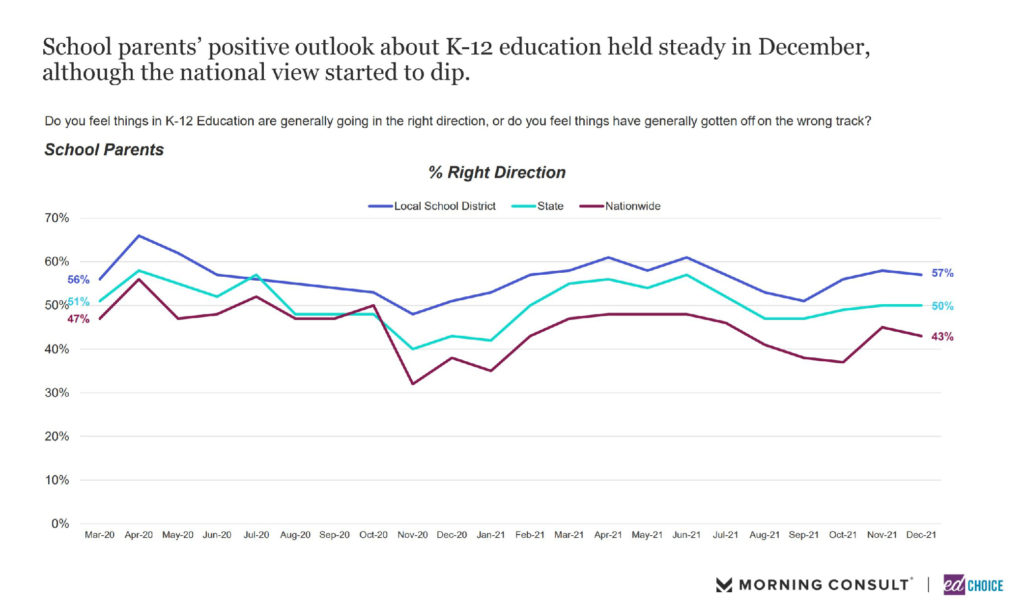

1. Parents and non-parents see K–12 education going opposite directions. While parents usually are more optimistic about the overall direction of K–12 education than the rest of the country—and that is true again this month—their optimism waned a bit in December. The share of parents who feel things in K–12 are going well at the local and national levels decreased slightly, while temperaments toward education at the state level remained even compared to November.

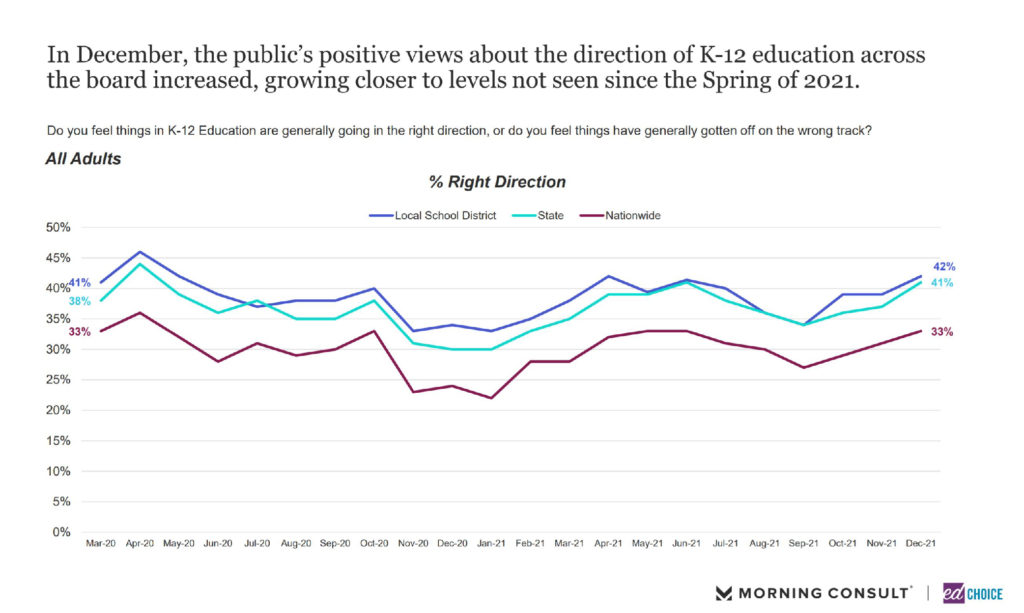

In contrast, sentiment about K–12 education among the general public is on the up-and-up. For the third consecutive month, the share of adults who think education is going the right direction on the state and national levels has increased over the previous month, and feelings about local education have jumped the most since September.

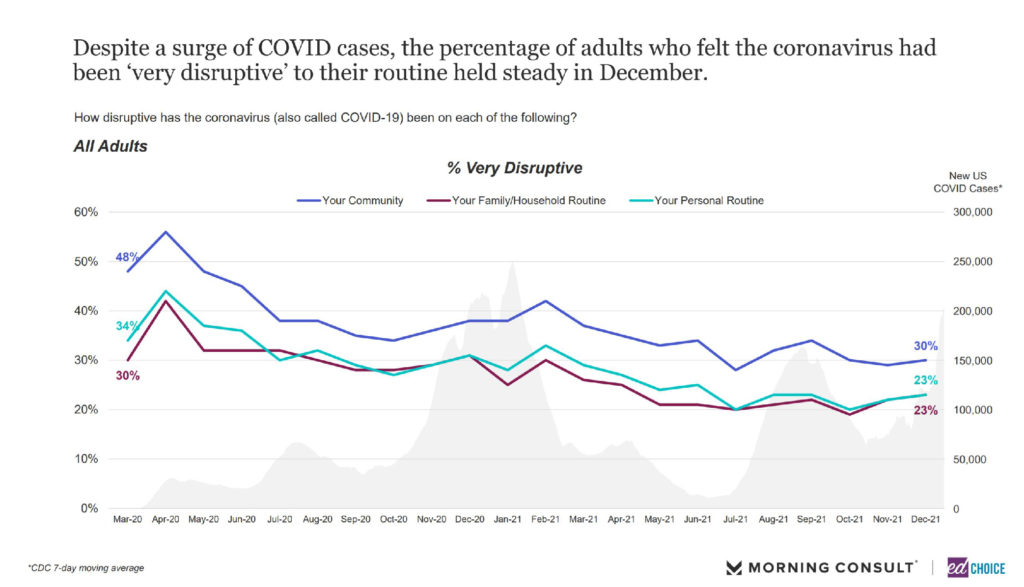

2. By mid-December, concerns about COVID-19 have not risen with surges in cases. Each month, we ask several questions about how the pandemic is affecting daily life, especially when it comes to how parents feel about schooling. While the United States saw a large jump in COVID-19 cases as the Omicron variant began to spread through the country, the share of people who felt the pandemic was “very disruptive” to their communities or daily lives increased only slightly compared to November.

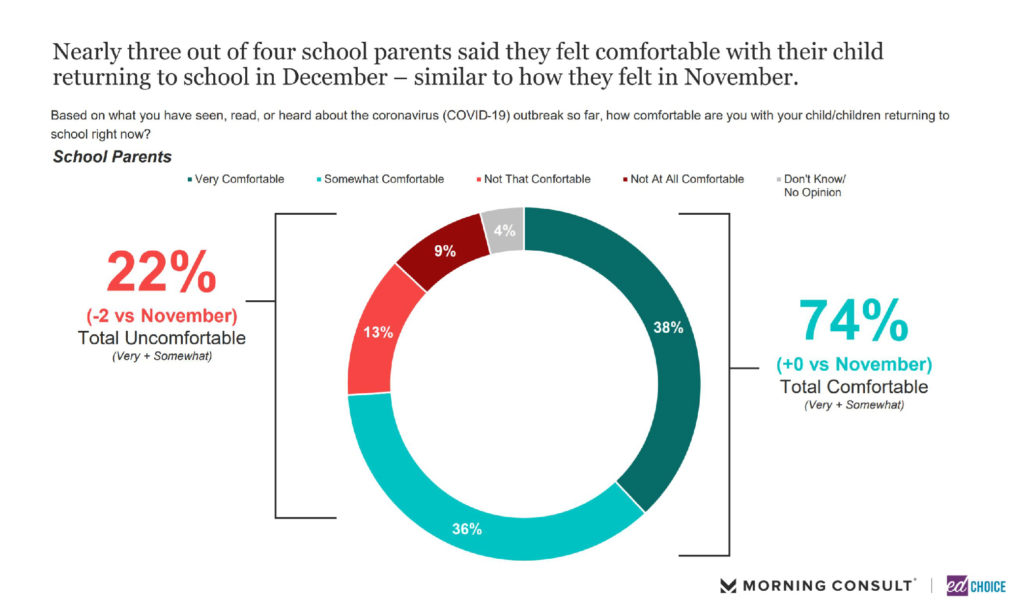

Likewise, the average parent was not any less comfortable with in-person schooling for their child in December than they were in November.

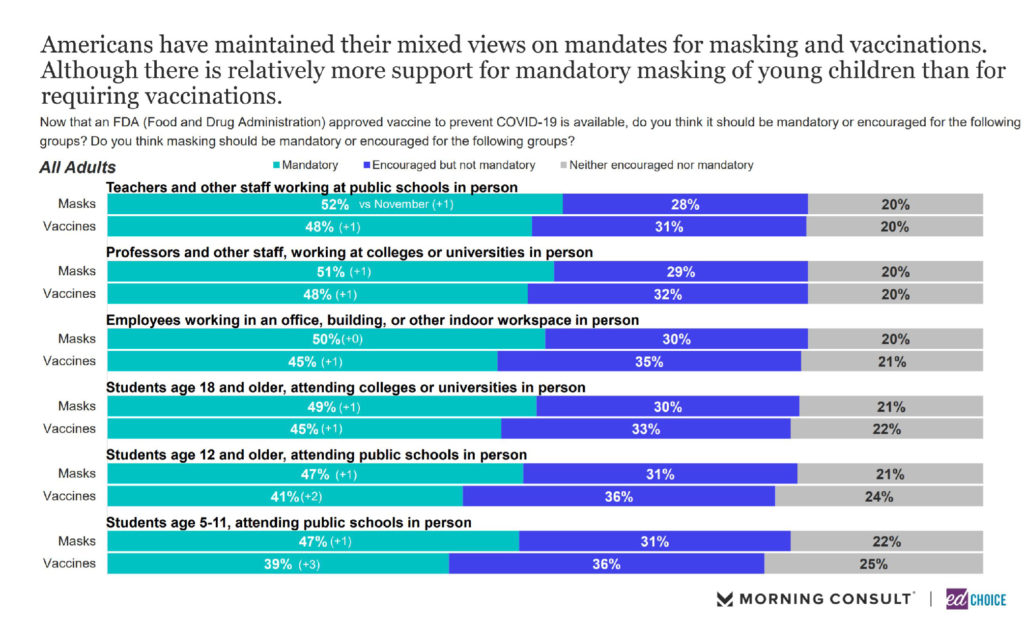

3. Certain anti-COVID measures may have become more important to those who value them. Public opinion on COVID safety policies also changed little in the early stages of the Omicron variant. The share of adults supporting mask mandates for a variety of populations and locations increased by no more than one percentage point. Vaccine mandate support increased by no more than one percentage point for adults but increased two and three points for students 12 and older and students aged 5–11, respectively.

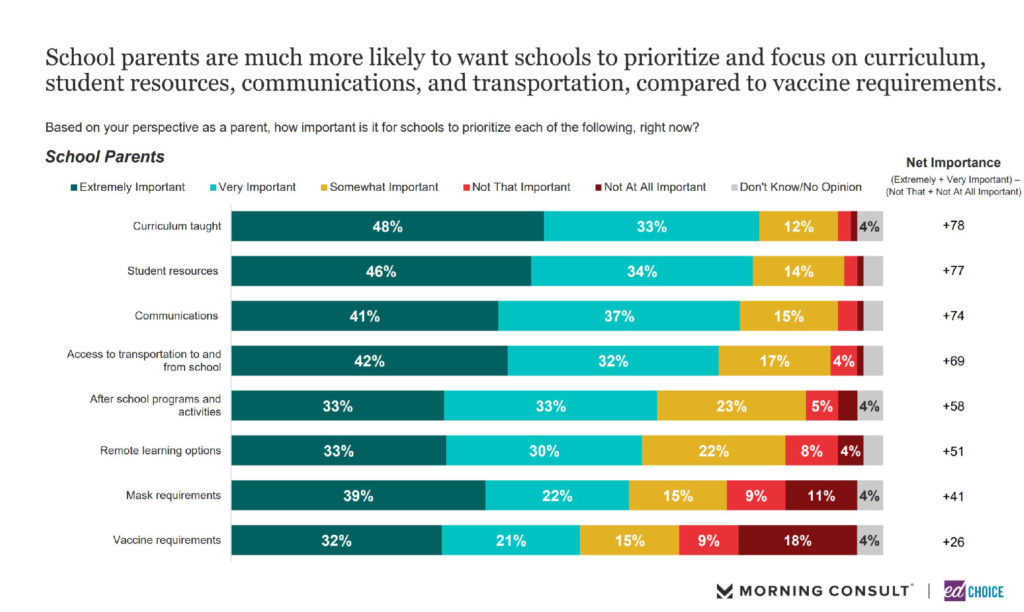

While the share of people interested in mask or vaccine mandates or policies did not increase much in December, the intensity of desire for COVID safety policies among those who are supportive appeared to grow. We offer parents a list of eight school activities and ask them to state how important they think each activity is. Six of those eight activities decreased in “net importance” (total “important” ratings minus total “not important” ratings). The two activities that became more important to parents were remote learning options (+6 percentage points) and vaccine requirements (+4 points).

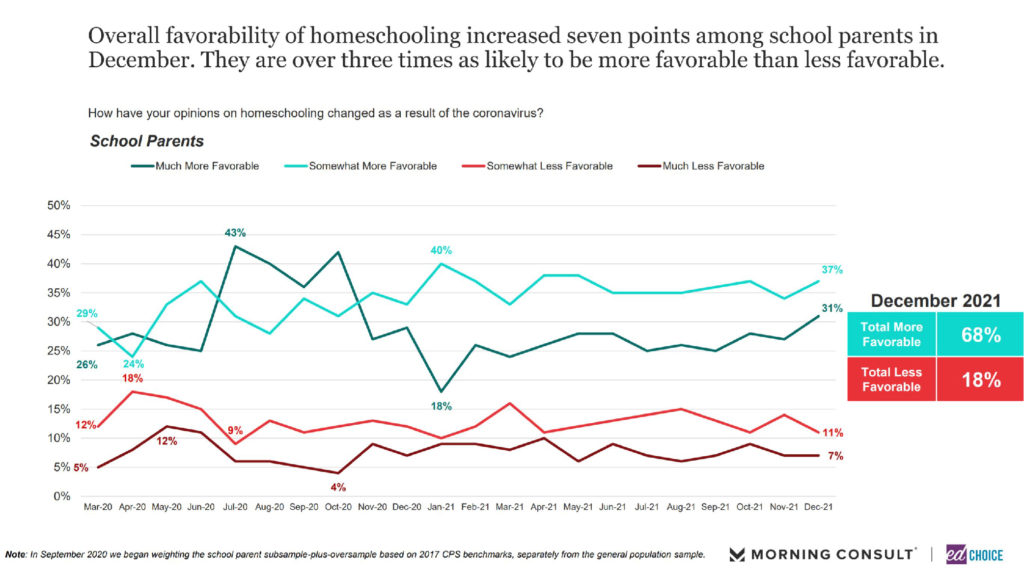

4. Support increased for education outside of traditional school settings. Since the early days of the pandemic, we have asked parents whether their perception of homeschooling has changed in light of COVID-19. After a year of volatility, answers have remained fairly consistent since the spring and summer of 2021. Though the share of parents who found homeschooling more favorably dropped in November, it rebounded in December. In fact, December 2021 was one of the highest homeschooling favorability rates since we began asking this question. Those identifying themselves as “much more favorable” toward homeschooling was at its highest point since October of 2020.

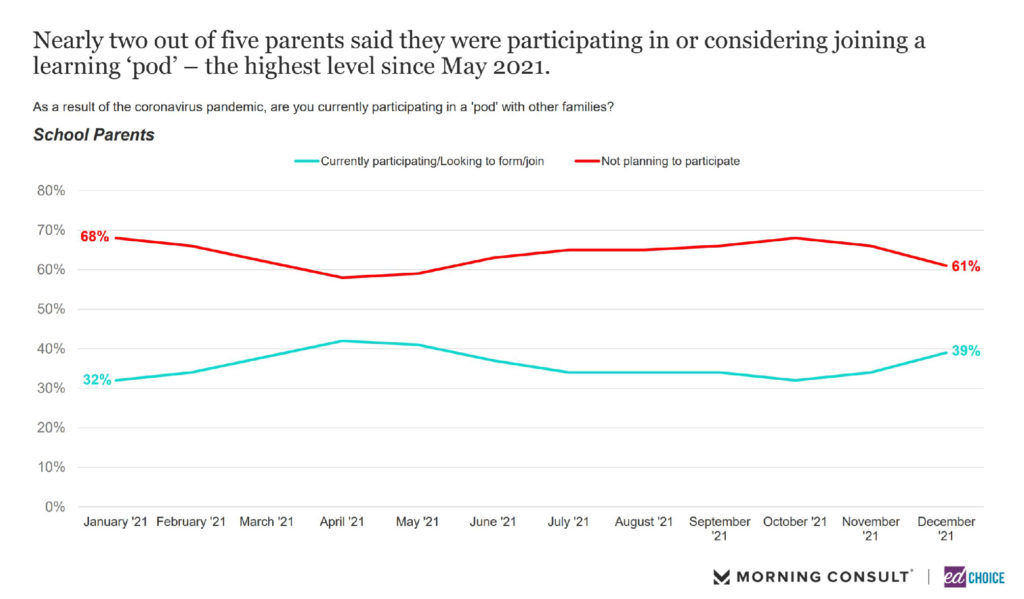

The percentage of parents at least interested in learning pods sat in the mid-30s for much of 2021. In December, we saw a five-point increase in interest compared to November, which was the highest level since May.

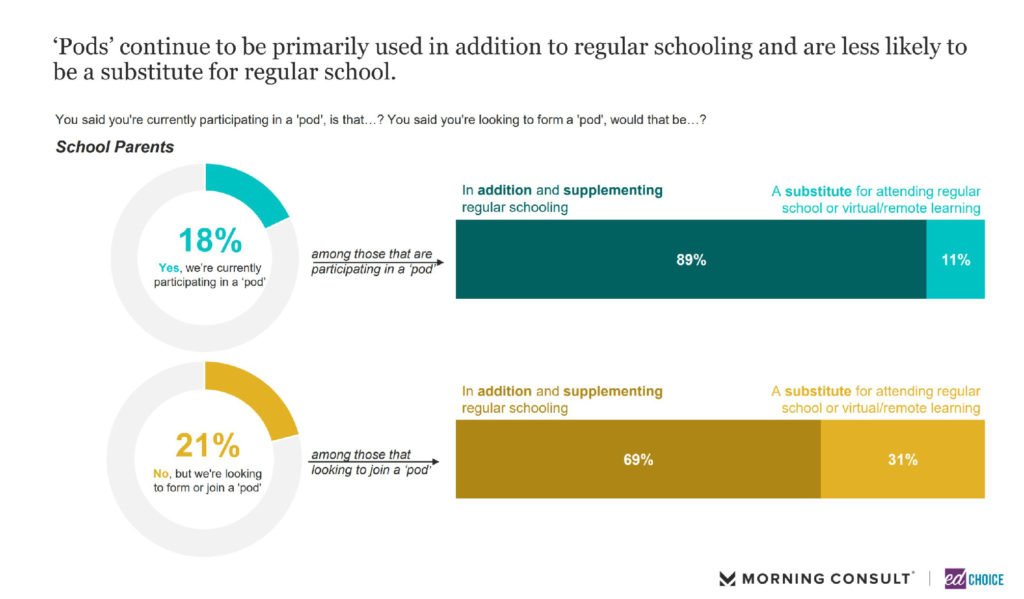

Parents who say they are either participating or expressing interest in joining learning pods most likely see them as supplementary to their children’s regular schooling. We tend to find roughly three out of four families currently participating in learning pods are using them to supplement regular school, while the remaining quarter uses them to substitute regular schooling. We tend to find about one-third of parents who were looking to join a learning pod see them as substitutionary.

Alongside the jump in pod interest, we found those currently in pods were eight percentage points more likely to identify their pod as supplementary to regular schooling than they did in November. Those not in but interested in pods went the other direction—they were two percentage points more likely than in November to think of pods as a replacement for regular schooling.

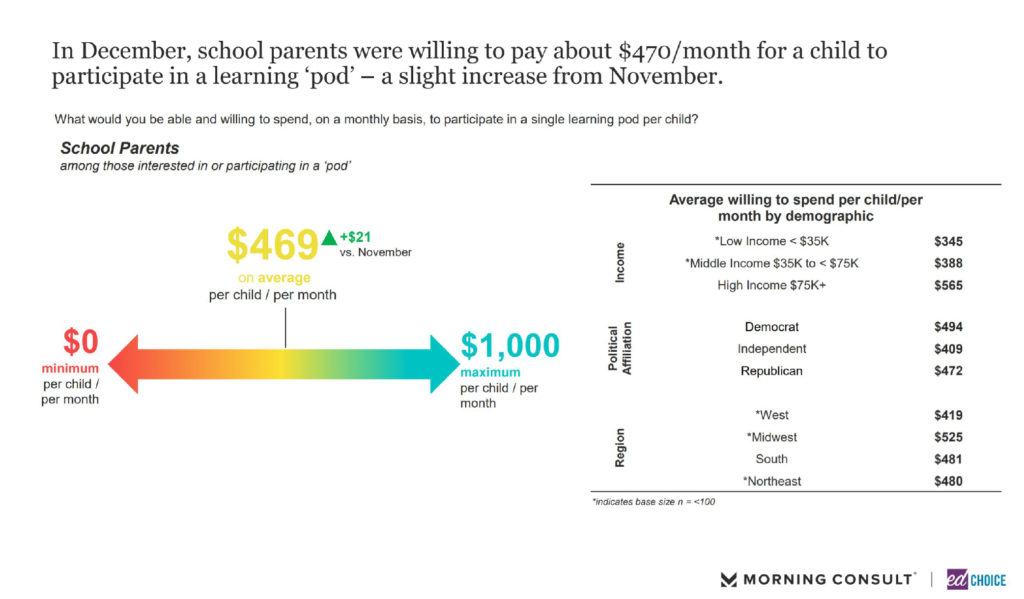

The intensity of interest in pods continues to tick upward as well. For the third consecutive month, the average willingness to pay for learning pods rose over the previous period. The average pod-inclined parent reported being willing to pay $469 per child per month to participate in a pod. While lower than the averages seen in spring 2021, we are seeing a similar trend in which the average willingness to pay rises as the school year carries on. Unlike spring 2021, however, those with annual household incomes above $75,000 are willing to pay substantially more than those making less than that amount.

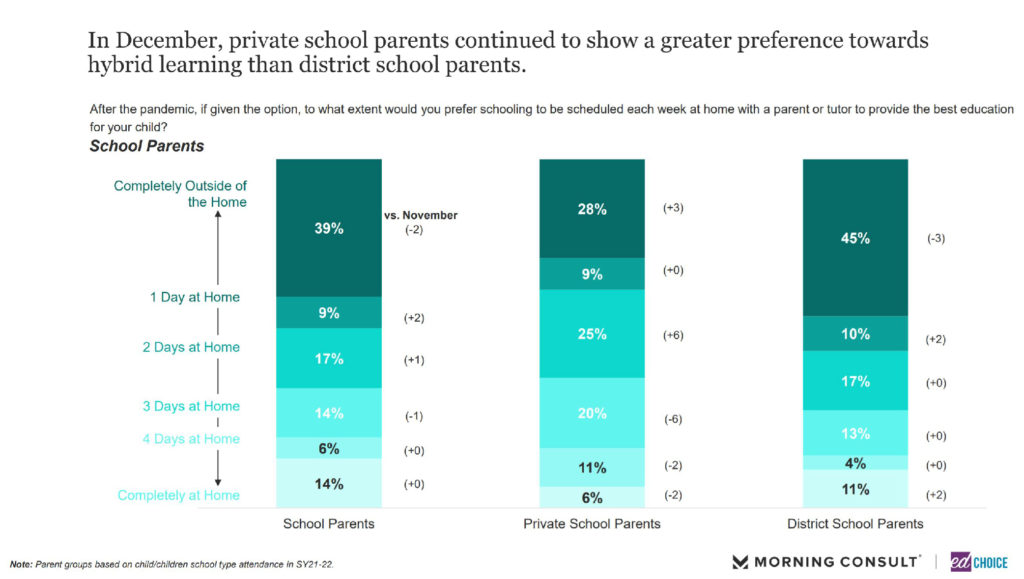

For many months now, we have seen a comfortable majority of parents state that their ideal school week after the pandemic would involve at least one day of learning taking place at home. Private school parents are especially likely to desire some kind of mix of at-school and at-home schooling. This month, two-thirds of private school parents preferred two to four days of education to take place at home.

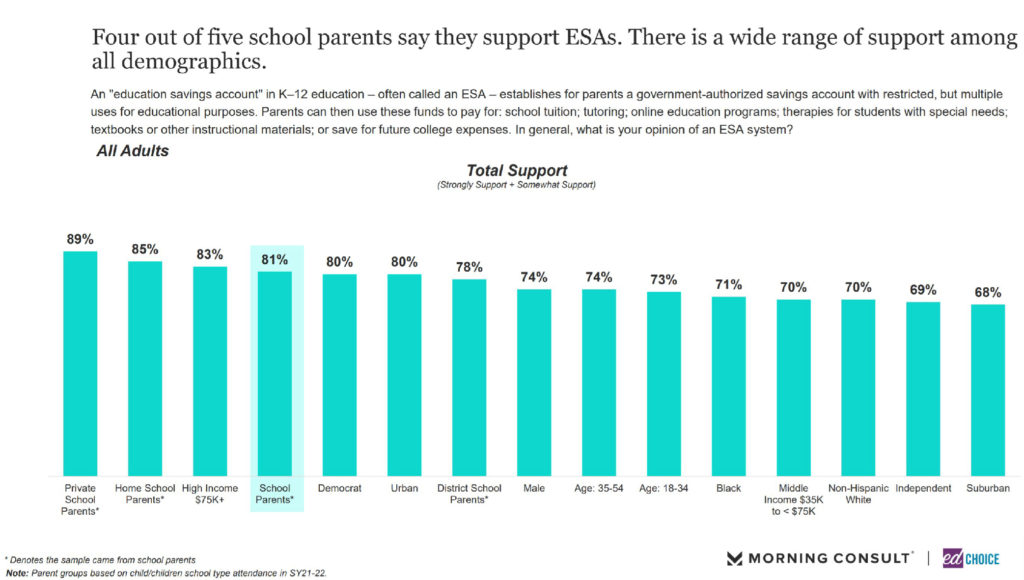

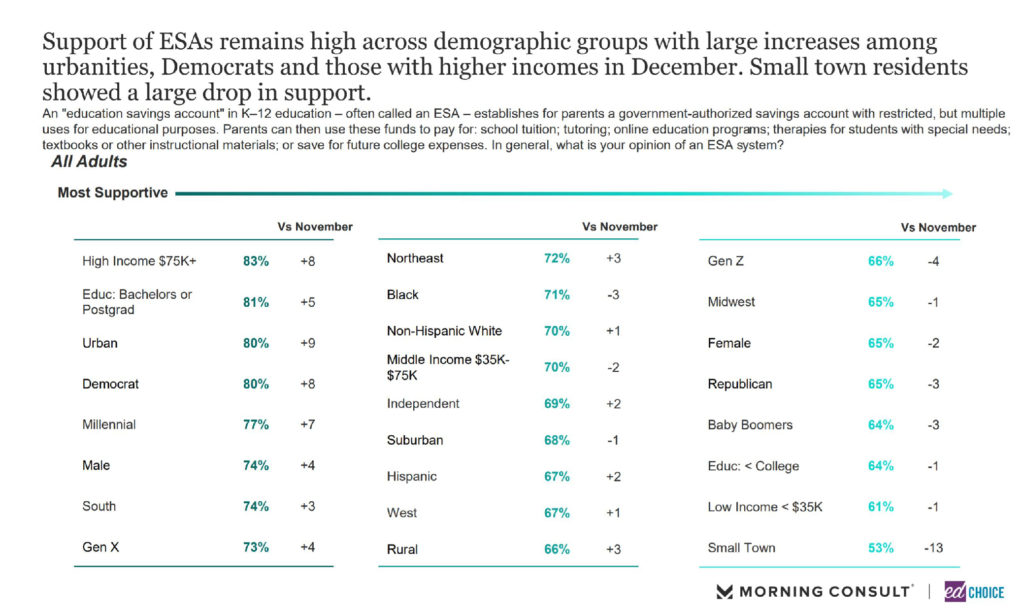

5. School choice remains a popular policy, especially among parents. Education savings accounts (ESAs) continue to be the most popular school choice policy, receiving support from 70 percent of adults and 81 percent of parents in December. This month, ESAs are particularly popular among educated, high-income households, urbanites, and Millennials.

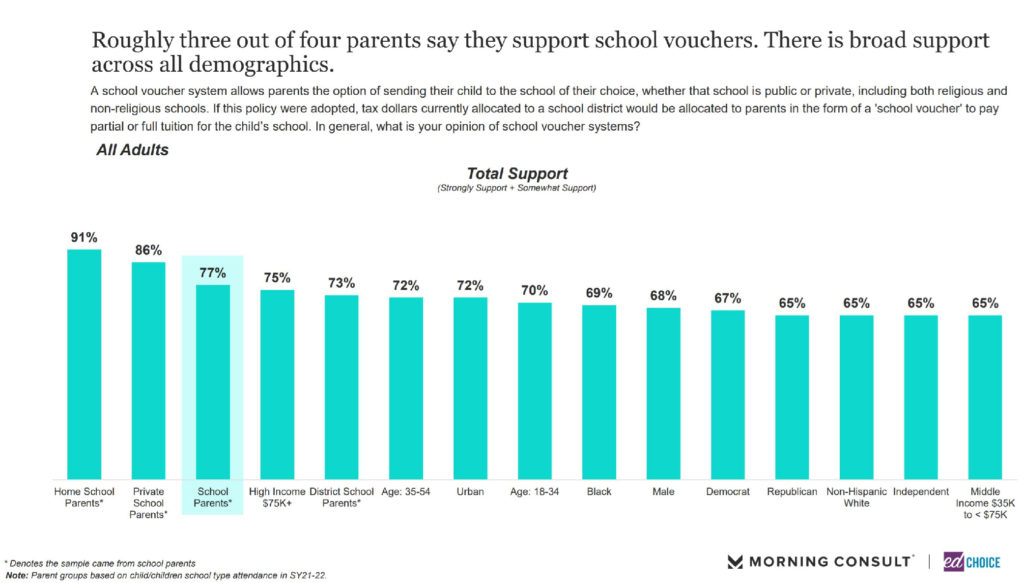

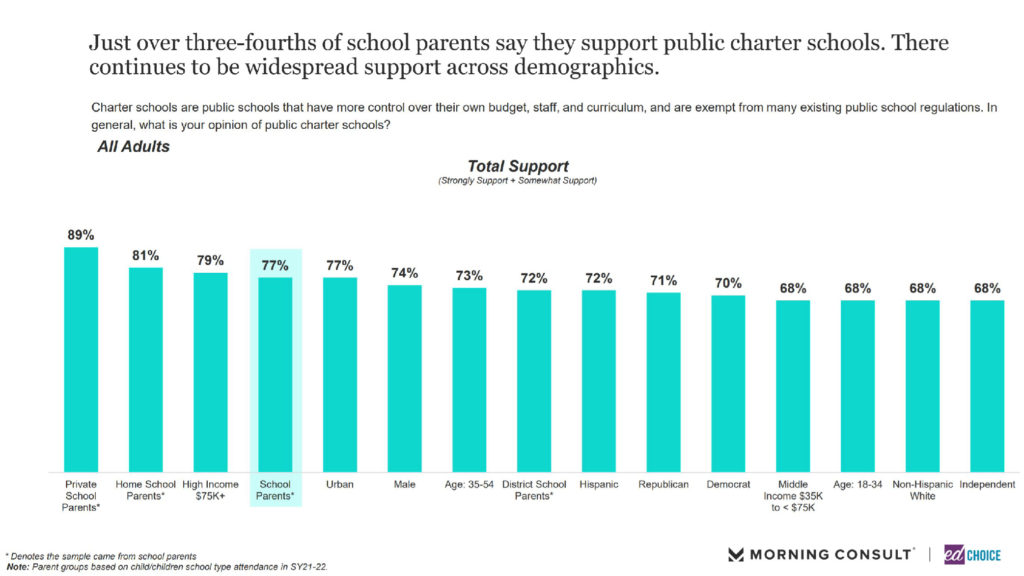

School vouchers and charter schools also receive strong majority support from both parents and the general population. Sixty-five percent of adults and 77 percent of parents indicate support for school vouchers, while 68 percent of adults and 77 percent of parents support charter schools.

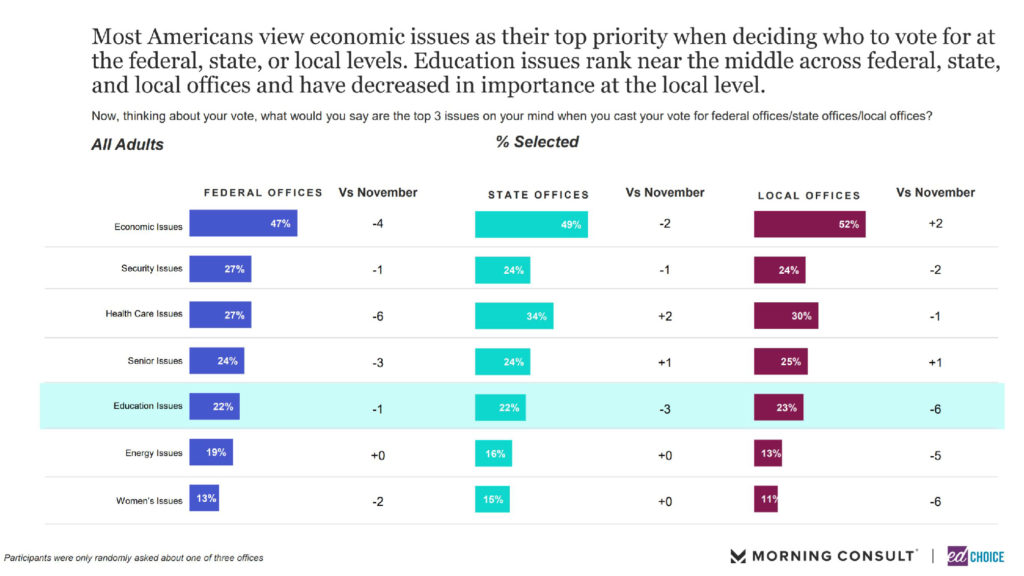

6. Compared to November, fewer people think of education issues as a major issue when it comes to elections. When asked to name their top three issues affecting their votes for various elected offices, less than a quarter of adults named “education issues.” At 22 percent, the share of people who consider education issues for federal elections is essentially unchanged from November. Those who named education a top-three for state and local offices declined by three and six percentage points, respectively. Most political issues at most levels saw declines in top-three interest, which may suggest that Americans’ interests became more diverse as the 2021 election season faded.

The parents who did name education as a top-three issue were especially likely to come from non-urban settings and have annual household incomes below $75,000. Black parents and parents who sent their children to private schools were the least likely to name education a top-three matter in elections.